.svg)

.svg)

.svg)

.svg)

.svg)

.png)

Sugar Market in Focus: Surplus Expectations & Price Pressure in October 2025

22th of December, 2025

by the Ingenius Team

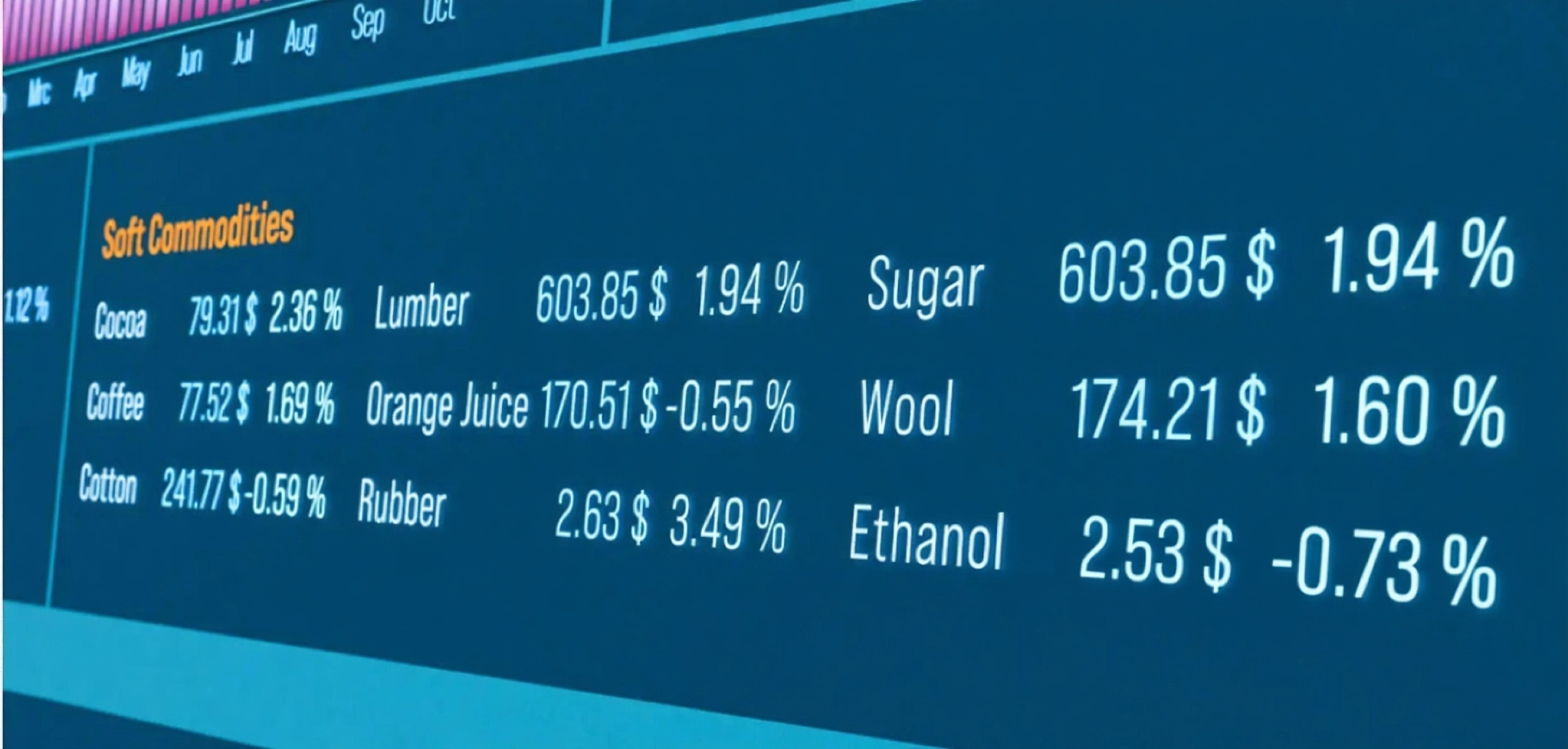

- In October 2025, raw sugar futures traded in the mid-teens, briefly dipping toward the 15–16 cents per pound range as markets reacted to shifting expectations for a 2025/26 surplus rather than any single confirmed supply outcome.

- After several years of deficits, the global sugar balance is now expected to swing back into surplus, though forecasts vary widely. Official estimates point to a modest surplus, while some private analysts project a much larger oversupply.

- India’s strong monsoon and expanded cane acreage are driving a sharp production rebound, reinforcing bearish sentiment even as uncertainty remains around exports and domestic policy.

- Europe’s largest sugar producer, Suedzucker, has cut its 2025/26 earnings guidance, citing weak sugar prices and margin pressure across the EU market.

- Price volatility remains elevated, shaped by sugarcane crushing rates, weather variability, and ethanol policy shifts in major producing countries—factors that continue to complicate procurement and risk management decisions.

The Forecast Shift: From Deficit to Surplus Expectations

The sugar market narrative pivoted sharply in October 2025. After multiple seasons defined by structural deficits, prices began to reflect expectations of a return to surplus in the 2025/26 marketing year.

As of late 2025, the International Sugar Organization (ISO) has revised its outlook from a small deficit earlier in the year to a relatively modest surplus of around 1.6 million metric tons. This marks a notable inflection point after years of tight balances but does not, on its own, imply a deep glut.

By contrast, private forecasters remain significantly more bearish. Analysts such as BMI have published projections suggesting a much larger surplus, with some estimates running above 4 million metric tons and as high as roughly 10.5 million metric tons. This wide divergence in forecasts not a single consensus number has been a primary driver behind the October sell-off in sugar futures.

Indian and Thai Output Rebounds Reinforce Bearish Sentiment

In October 2025, sugar futures softened toward the mid-teens as markets digested the scale of production rebounds across Asia and South America. After years of constrained supply, rising output from India and Thailand has reinforced expectations of a looser global balance in 2025/26.

India’s recovery has been particularly influential. Favorable monsoon conditions and increased cane planting are expected to lift production by roughly 20–25% year over year, pushing output to around 35–35.3 million metric tons. This rebound alone has materially altered the supply outlook, even as questions remain around export limits and domestic stock management.

Thailand is also emerging as a key contributor. Following prior drought-impacted seasons, its 2025/26 crop is now forecast to rise by approximately 10–12%, with output expected to reach just over 11 million metric tons further easing regional supply constraints.

.png)

The Domino Effect from Other Major Producers

The global supply picture is being reshaped most decisively by Brazil. The country’s Center-South region is on track for record or near-record production of roughly 45 million metric tons in 2025/26, reflecting improved yields and sustained milling capacity despite earlier weather challenges.

Taken together, rising output from Brazil, India, and Thailand has reversed the market psychology that dominated recent seasons. After multiple years of deficits stretching back to 2019/20, markets are now trading on expectations of a return to surplus, even though official estimates still point to only a modest excess.

This gap between official balances and more aggressive private forecasts has amplified price sensitivity. Any deviation whether weather-related disruptions, ethanol policy changes, or logistical constraints could still quickly tighten the balance and trigger renewed volatility.

Financial Outlook Reflects Market Pressure in Europe

Europe’s sugar sector is already feeling the impact of weaker prices. Suedzucker, the region’s largest producer, has reduced its 2025/26 earnings guidance, citing persistent pressure from low sugar prices and softer demand across the EU.

While cost-control efforts and operational efficiencies have helped limit downside risk, they have not fully offset margin compression in the sugar segment. The company’s more cautious outlook underscores the broader challenge facing European producers as global supply growth weighs on pricing power and export competitiveness.

For market participants, Suedzucker’s guidance serves as a reminder that even a modest surplus on paper can translate into meaningful earnings pressure when prices remain subdued.

.png)

Evolving Supply-Demand Dynamics Shape Procurement Strategies

With 2025/26 balances still subject to wide forecasting ranges, procurement and finance leaders must operate in an environment defined less by certainty and more by scenario management.

As of late 2025, official data points to only a small surplus, while private models warn of a far larger glut. This divergence makes agile risk management, flexible sourcing, and disciplined hedging essential rather than optional.

Weather variability, shifting ethanol mandates, and policy decisions around exports will continue to influence outcomes. In this context, AI-powered forecasting and analytics remain key, enabling teams to stress-test assumptions, monitor inflection points, and respond faster to market shifts.

Why It Matters

With official data pointing to only a modest surplus and private forecasts warning of a much larger glut, sugar buyers are operating in a market driven as much by expectations as by fundamentals.

This is where AI-driven tools like InGenius Forecaster matter. By combining machine learning with real-time market data, IG Forecaster helps procurement and finance teams move beyond static assumptions and model multiple price and supply scenarios as conditions evolve.

In a market this volatile, predictive insight, faster signal detection, and disciplined risk planning remain key to protecting margins especially when weather, policy shifts, or ethanol economics can quickly flip the narrative.

Nos produits incluent Prévisionniste IG pour des prévisions de marché précises et Portefeuille IG pour des stratégies de placement plus intelligentes.