.svg)

.svg)

.svg)

.svg)

.svg)

Silver's Strategic Shine: A Practical Guide for Sourcing and Risk Management

8th of December, 2025

by the Ingenius Team

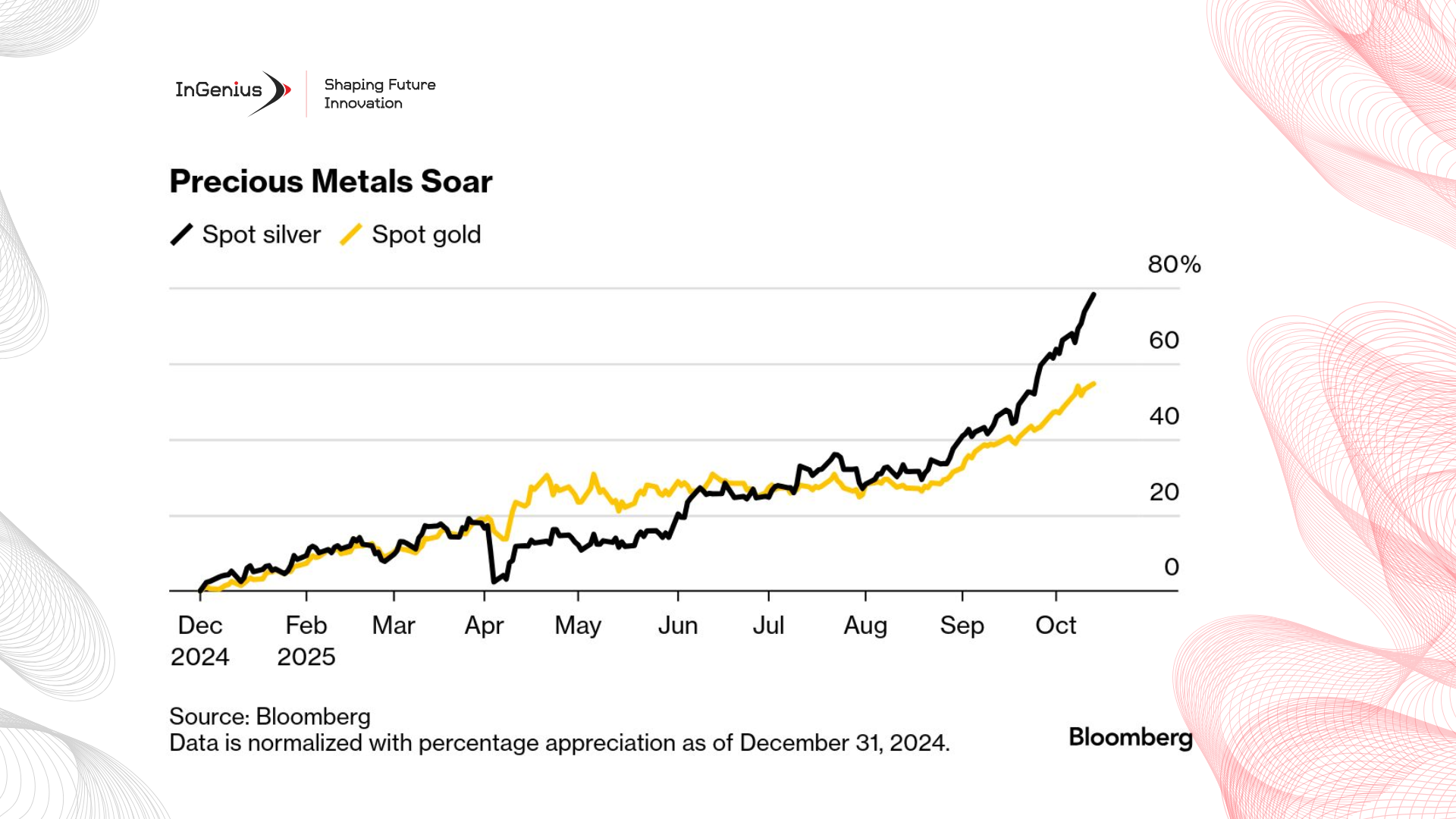

- Silver’s 2025 rally remains closely tied to gold’s strength, with silver trading in the $27–$30 range late in the year as rate expectations and geopolitical tensions keep safe‑haven metals elevated.

- Silver ETF inflows cooled in mid‑2025, even as gold continued attracting most central‑bank demand, highlighting a more cautious but still supportive investment environment.

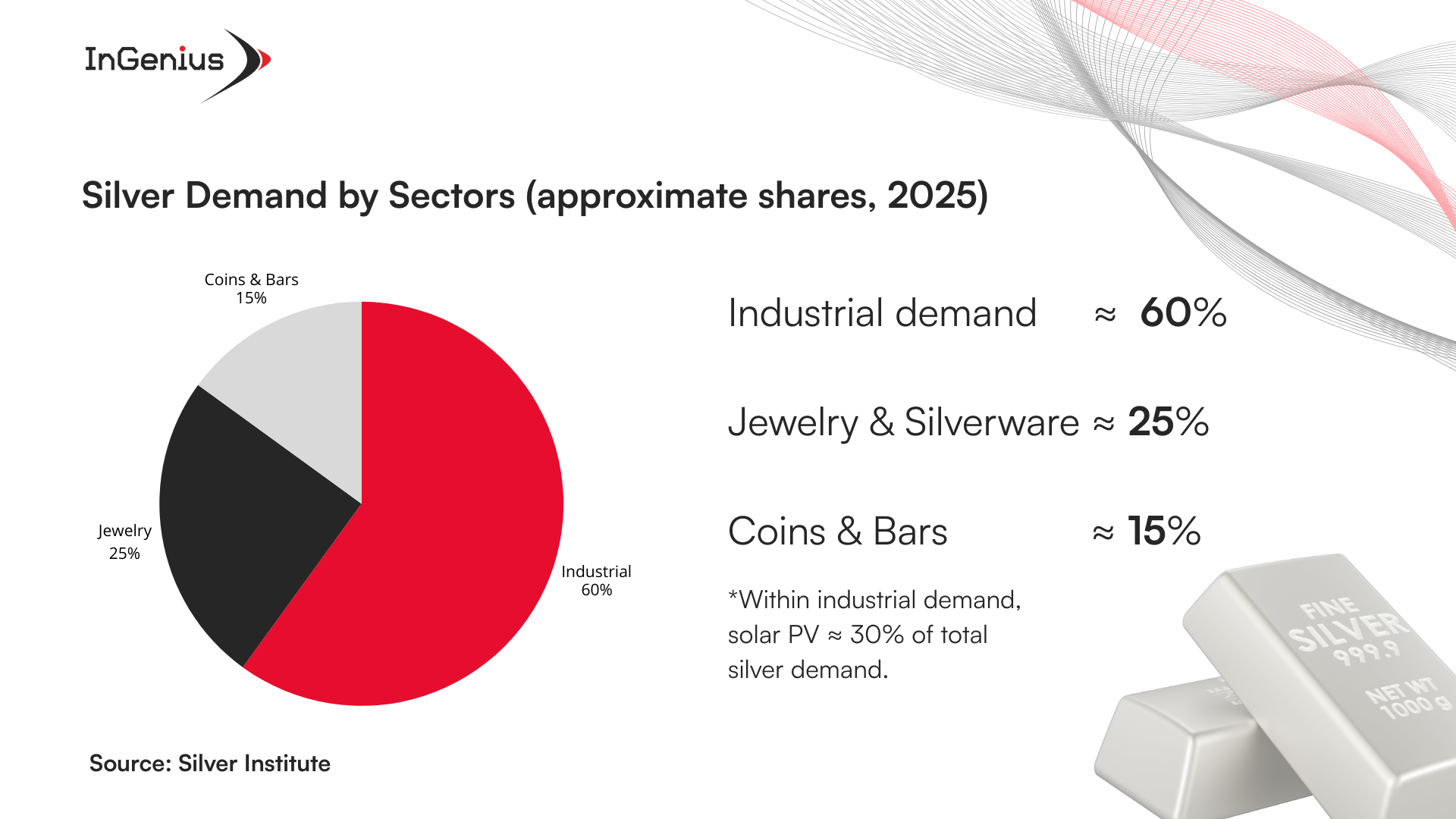

- Industrial demand remains silver’s backbone, with photovoltaics alone consuming over 180 million oz (≈ 30% of demand in 2025).

- Silver remains in structural shortage, with a ~140 million oz deficit projected for 2025, the fifth consecutive year of undersupply.

- Markets remain volatile heading into Q4 2025, shaped by Fed rate‑cut uncertainty, tariff debates, USD fluctuations, and U.S. election risk.

Silver’s Rally Fueled by Gold’s Strength

Silver’s 2025 performance has closely mirrored gold’s resilience, with gold holding above $2,300/oz through much of the year (World Gold Council Q3 2025 Report). Given their historic 0.8–0.9 correlation (LBMA Correlation Data), silver stabilized around $27–$30 by late 2025.

This momentum wasn’t linear. Silver saw sharp swings mid‑year as markets responded to alternating Federal Reserve policy signals, soft data, and geopolitical tension. Each pullback found support, reflecting continued safe‑haven demand.

Collectively, these dynamics reinforce silver’s dual identity — both a monetary hedge and a strategic industrial commodity.

Central Banks and ETFs Boost, but Also Complicate Silver’s Momentum

Mid‑2025 saw a slowdown in silver ETF inflows (Metals Focus Oct 2025), even as gold continued to dominate institutional

accumulation (World Gold Council, Central Bank Gold Survey 2025).

High‑profile purchases , like the Saudi Central Bank’s $40 million commodity‑linked

exposure (Reuters June 2025 coverage) , supported sentiment but did not signify broad central‑bank silver buying.

Gold remains the primary reserve metal.

For procurement leaders:

- ETF flows shape liquidity and price momentum.

- Gold‑heavy central‑bank policies bolster the wider precious‑metals complex.

- Silver’s investment‑linked volatility remains high,

making ETF trend tracking essential for risk planning.

Industrial Demand Keeps Silver in the Spotlight

Silver’s strategic importance in 2025 centers on industrial use. More than 50% of global demand now derives from industry, led by photovoltaics (PV). According to the Silver Institute 2025 Interim Review, PV alone consumes over 180 million ounces annually (≈ 30 % of total demand).

Ongoing drivers include:

- EV power electronics and battery systems (IEA Global EV Outlook 2025)

- Advanced semiconductors and medical instrumentation

- Power distribution and sensor technologies linked to energy efficiency standards

Although jewelry and silverware sales softened amid higher prices, green technology’s surge has kept overall consumption robust. For procurement, silver is no longer a passive hedge but an essential industrial input with limited substitution options — underscoring the need for long‑term sourcing partnerships.

Supply Constraints and Market Deficits

Global mine supply rose only ~2 % in 2025 (GFMS Metals Outlook Nov 2025), continuing to trail demand. The Silver Institute projects a ~140 million oz deficit , the fifth straight year of undersupply.

Recycling has inched up but remains insufficient to relieve deficits. Moderate improvement may arrive in late 2026 as new Mexican and Peruvian projects come online (Mining Journal Oct 2025), yet overall tightness will persist.

For supply chains:

- Structural shortage and price volatility will extend into 2026.

- Strategic contracting and hedging outperform spot buying in this market.

Strategic Considerations Amid Market Uncertainty

Procurement leaders now operate within a volatile macro matrix, federal rate‑cut speculation, USD fluctuations, trade policy debates, and U.S. election‑driven uncertainty through Q4 2025 (Reuters Markets Coverage, Dec 2025).

Adaptive organizations are investing in:

- Real‑time pricing analytics and data feeds (LBMA Data Portal)

- AI‑assisted price forecasting tools (InGenius IG Forecaster)

- Contract diversification and multi‑supplier partnerships

- Scenario‑based hedging models for currency and metal risk

Data‑driven risk management is now a core capability for procurement and finance leaders.

.png)

Why It Matters

Silver sits at the crossroads of monetary value and industrial necessity. Its dual role , as a financial hedge and an irreplaceable clean‑energy metal , makes it a strategic factor for supply chain resilience.

Understanding demand trends and deficits, tracking macro drivers, and embedding scenario planning into sourcing decisions helps organizations stabilize margins and reduce volatility exposure.

With early 2026 expected to test the pace of supply recovery, adaptive sourcing and data‑driven risk strategies will define competitive advantage in the year ahead.

Nos produits incluent Prévisionniste IG pour des prévisions de marché précises et Portefeuille IG pour des stratégies de placement plus intelligentes.